Sue Britton

CEO, FinTech Growth Syndicate

In just a few short years, fintech has become a large and successful new market category in technology and financial services in Canada creating tens of thousands of jobs and attracting the attention of global markets for our talent and technology.

Despite the success in the growth of new entrants and increasing adoption of their products by consumers and businesses, incumbents are still preoccupied with maintaining margins and prioritizing slow legacy technology modernization projects, over partnering with smaller new companies, becoming more agile and lowering costs, or creating new business models. For the most part, your bank has not changed what it does for you today, other than to provide a more enhanced “digital experience.”

Do incumbent financial institutions still have the benefit of a large customer base to fend off competition?

No one would argue that we need stable, low-risk and secure financial services institutions in Canada, it is a key driver of our economic well-being as a country. But “if we do what we have always done, we will get what we always got” and the other undisputed fact is that the technology that created our secure systems a decade or two ago, cannot keep financial institutions relevant today. We need business model innovation. Executives in incumbent organizations need to look at their industry through another lens and reinvent how they make money. The new fintech market is an indicator for business model changes, lower fees, more value for consumers, and less friction.

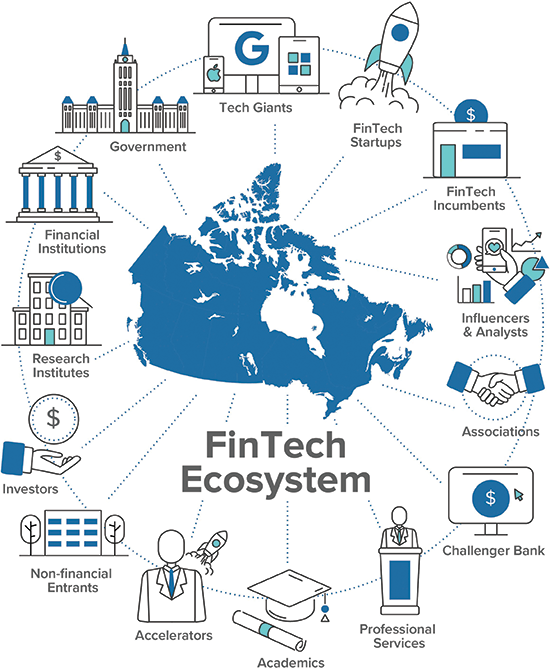

The fintech ecosystem represents what is possible. It provides a realistic view on how technology is constantly adapting to the needs of the consumer, as new products and fintechs are launched. As tech giants such as Facebook, Apple, and Amazon launch fintech products in Canada and leverage their own large customer base for faster adoption, the need for true innovation through strategic partnering within the fintech space becomes a necessity. Amazon’s new credit card launched recently in Canada, for instance, introduces massive competition for incumbents.

Do incumbent financial institutions still have the benefit of a large customer base to fend off competition? How fast will competition arrive and change the landscape in Canada? The answer is not clear, but for sure, innovation needs to move faster.

At FinTech Growth Syndicate (FGS), our passion is to help innovators succeed. One way that can happen faster is through partnerships within the ecosystem. Over 1,200 start-ups and scale-ups in Canada are catalysts for growth, and knowing and working with them is key to fueling the innovation process. These companies provide a map of what customers and businesses need and are solutions to the problems they have. As an incumbent, we believe that you can’t have innovation without research. Research is table stakes for transformation teams, or as we like to call them, “transformationists,” and by bringing the ecosystem and innovators together, stakeholders become not only collaborators, but enablers in the ecosystem.

When we started FGS, our first blog was about 3 people who walk into a bar; an investor, a banker and a fintech start-up founder. The investor says to the bartender, “I’ll have what they are having,” and the banker says, “I’ll have what they are having” — you get the picture. Today we would have the investor, the banker, the fintech founder, the tech giant, the challenger bank, and possibly a stranger whom we don’t yet know — maybe the Telco? Stay tuned.